TL;DR — Shakepay Review 2026

Shakepay is ranked #8 on our list of best crypto exchanges for Canadians with an 8.8/10 rating. It’s Canada’s one of most popular Bitcoin app with 1.5 million users, and it’s come a long way since I first signed up years ago. It’s now CIRO-registered, a member of Payments Canada, and as of April 2026 offers bitcoin-backed loans, features no other Canadian crypto app was offering when I started testing exchanges back in 2016. The platform still only supports Bitcoin and Ethereum, and the spread runs 1.5% to 2.5%, so it’s not the cheapest option if you’re trading frequently. But for Canadians who want a dead-simple way to buy BTC, earn bitcoin cashback on everyday spending, and now earn interest on their cash balance, Shakepay is hard to beat as a starting point. Use this link to get $20 free when you trade $100 or more.

Shakepay Quick Facts

| Detail | Info |

|---|---|

| Founded | 2015, Montreal, QC |

| Founders | Jean Amiouny & Roy Bregg |

| Canadian users | 1.5 million+ (as of 2026) |

| Coins supported | Bitcoin (BTC) and Ethereum (ETH) only |

| Trading spread | 1.5% to 2.5% (market conditions vary) — Verified June 17, 2026 |

| CAD deposit fee | Free |

| CAD withdrawal fee | Free (Interac e-Transfer, instant) |

| Crypto withdrawal fee | Free (Shakepay covers network fees) |

| Interac deposit minimum | $5 CAD |

| Interac deposit maximum | $10,000 CAD |

| Wire transfer minimum | $10,000 CAD |

| Deposit methods | Interac e-Transfer, wire transfer |

| FINTRAC MSB | Yes — Verified June 17, 2026 |

| CIRO registered | Yes (investment dealer, January 2025) — Verified June 17, 2026 |

| Payments Canada member | Yes (first crypto company, May 2025) — Verified June 17, 2026 |

| Visa card | Yes (tiered BTC cashback, up to 4% during promotions) |

| Bitcoin-backed loans | Yes (launched April 2026, 9.5% APR, up to $50K CAD) |

| Interest on cash | Yes (up to 3.75% APY, paid in BTC weekly) |

| Trustpilot rating | 3.1/5— Verified June 17, 2026 |

| App Store (iOS) | 4.7/5 — Verified June 17, 2026 |

| Google Play | 4.5/5 (12,000+ reviews) — Verified June 17, 2026 |

| Referral bonus | $20 free on first trade of $100+ CAD |

| Canada only | Yes — all 13 provinces and territories |

Shakepay Pros and Cons

-

-

Pros & Cons

- Free CAD deposits and withdrawals via Interac (rare among exchanges)

- Shakepay covers crypto network/mining fees on withdrawals

- CIRO-registered investment dealer (January 2025) and Payments Canada member (May 2025)

- Visa card with tiered BTC cashback (up to 4% during promotions)

- ShakingSats: earn free BTC daily just by shaking your phone

- Shakepay Interest: up to 3.75% APY on CAD balance, paid in BTC weekly

- Bitcoin-backed loans launched April 2026 (first regulated option in Canada)

- Incredibly beginner-friendly app (4.7/5 on iOS)

-

Fees

- Free crypto withdrawals

- Free CAD deposit/withdrawal (Interac and wire)

- Trading fee spread: 1.2% – 2.5%

-

Coins

Bitcoin and Ethereum

If Shakepay sounds like the right fit after that breakdown, open an account here and get $20 free on your first $100+ trade. Not sure Shakepay is right for you? Take our exchange quiz to find your best match.

Is Shakepay Legit and Safe for Canadians in 2026?

Yes, Shakepay is legitimate and among the most regulated crypto platforms available to Canadians. It holds FINTRAC MSB status, registered with CIRO as an investment dealer in January 2025 (the first Quebec-based crypto company to do so), and became the first crypto-native firm admitted to Payments Canada in May 2025. Client funds are stored in cold storage with insurance coverage, and 2FA is supported.

When I first started reviewing Canadian exchanges around 2016, the regulatory question was always murky. FINTRAC registration was the minimum bar, and most platforms treated it as a checkbox. Shakepay has gone well beyond that now.

The CIRO registration is significant. CIRO (the Canadian Investment Regulatory Organization) is the national self-regulatory body overseeing investment dealers in Canada. Most crypto platforms in Canada are registered only as money service businesses under FINTRAC. Being a CIRO-registered investment dealer puts Shakepay in a different category entirely, with stricter reporting requirements and audited financials.

Quebec’s AMF (Autorité des marchés financiers) granted Shakepay a 3-year exemptive relief decision, which is what allowed the bitcoin-backed loan product to launch in April 2026.

On security: Shakepay stores the majority of customer assets in cold storage, with hot wallets used only for day-to-day liquidity needs. The platform supports two-factor authentication via authenticator apps, FaceID and biometrics on mobile, and email confirmation on withdrawals. I always recommend setting up 2FA on your email account as well, since that’s typically the weakest link if someone gets into your inbox.

One genuine gap worth naming: Shakepay still does not publish the exact percentage of assets held in cold storage, and the details of their insurance policy are not publicly disclosed. That lack of transparency has been a criticism for years. It does not disqualify the platform, but if you are holding a significant amount, move it to a hardware wallet. That applies to every exchange, not just Shakepay.

What Is Shakepay’s Track Record in Canada?

Shakepay launched in Montreal in 2015, grew to 1 million Canadian users by early 2025, and now serves 1.5 million Canadians as of 2026. It has never suffered a major hack, has expanded from a simple Bitcoin broker into a personal finance platform, and hit multiple regulatory milestones that no other Canadian crypto company had previously achieved.

Shakepay in Canada: Key Milestones

| Year | Milestone |

|---|---|

| 2015 | Founded in Montreal by Jean Amiouny and Roy Bregg |

| 2015 | FINTRAC MSB registration — one of the first Canadian crypto platforms to register |

| 2021 (November) | Shakepay Visa card launched — first Canadian exchange to offer BTC cashback on everyday purchases |

| 2024 | Crossed 1 million Canadian users |

| January 2025 | CIRO investment dealer registration — first Quebec-based crypto platform to achieve this |

| Q1 2025 | Shakepay Interest launched — up to 3.75% APY on CAD balance, paid in BTC weekly |

| Q1 2025 | Large trade optimization rolled out — improved spreads on larger transactions |

| Q1 2025 | Bill payments, direct deposit, and USD/USDC accounts added |

| May 2025 | First crypto-native company admitted to Payments Canada |

| 2026 | Reaches 1.5 million Canadian users |

| April 21, 2026 | Bitcoin-backed loans launched — first regulated BTC-collateralized loan product in Canada (9.5% APR, $50K CAD cap, AMF-approved) |

Ten years in, no major security incident, consistent regulatory progress, and a product roadmap that has actually delivered. That’s a meaningful track record for a Canadian crypto platform.

How Do You Sign Up and Verify Your Account on Shakepay?

Signing up takes about 5 minutes. Verifying your identity requires a government-issued photo ID (driver’s licence or passport) and a short selfie video — you’ll read digits aloud on camera. Auto-approval usually completes within minutes, but manual review can take up to 7 days if the auto-check doesn’t pass on the first try.

Here’s what the process actually looks like, step by step:

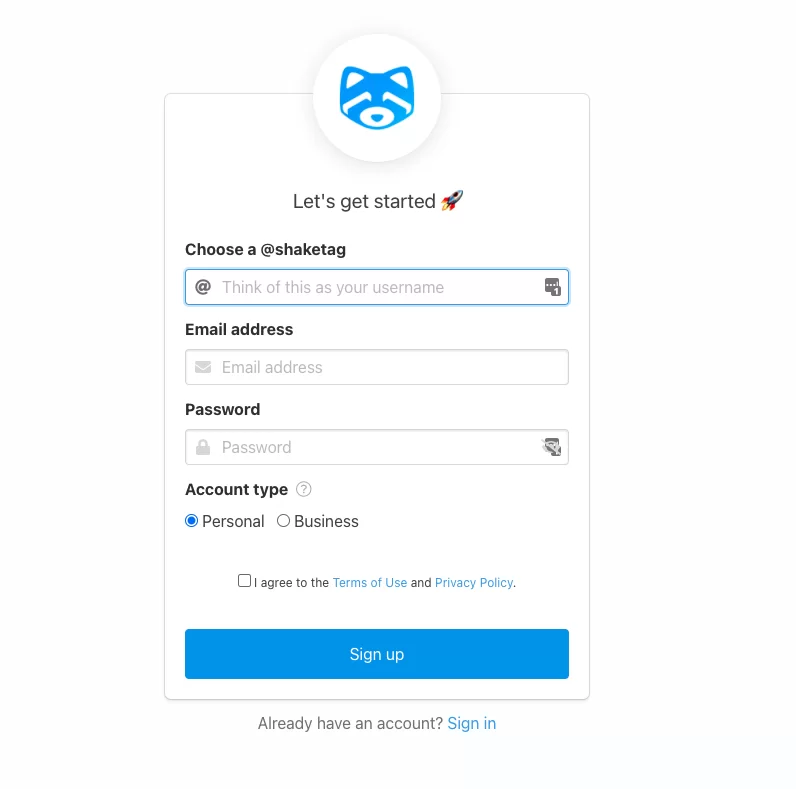

- Create your account. Enter your email, set a password, and choose a Shaketag — this is your unique username, used for sending crypto to other Shakepay users for free. Pick one you like because you can’t easily change it later.

- Upload your government ID. A Canadian driver’s licence or passport works. The app walks you through capturing both sides. Ensure the photo is clear and the ID isn’t expired.

- Record a short selfie video. You’ll see a sequence of digits on screen and need to say them aloud while keeping your face within the frame. It sounds odd the first time but takes under a minute. This is Shakepay’s liveness check — it replaced the old static selfie-with-ID process and is actually more secure.

- Wait for verification. If auto-approval goes through, you can deposit funds immediately. If it goes to manual review, expect up to 7 business days. During busy market periods, manual reviews sometimes take longer.

One thing worth knowing: if verification is delayed and you’re trying to buy during a price move, that window is just gone. I’ve seen this come up repeatedly in Reddit complaints from Canadians who signed up during a bull run and couldn’t get verified fast enough. If you’re planning to use Shakepay, sign up and verify before you need to buy, not during a market event.

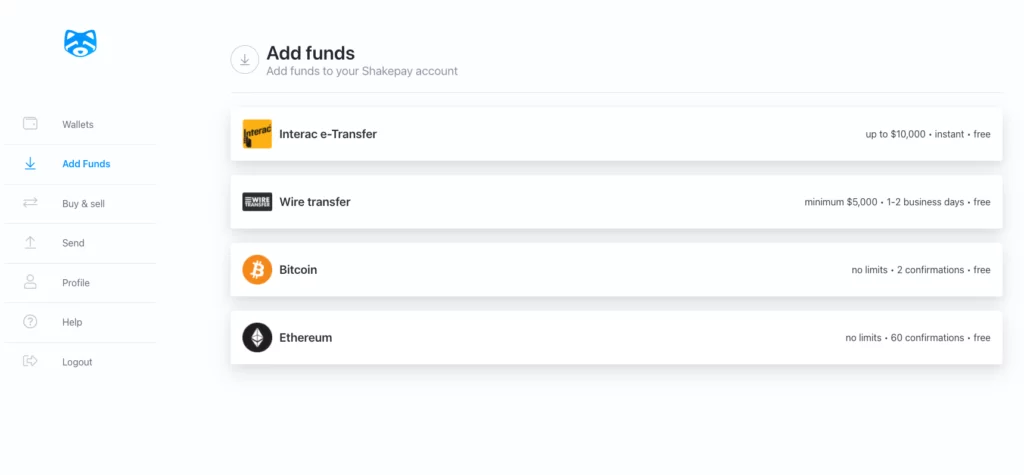

How Do You Add Funds to Shakepay?

The best and most common method is Interac e-Transfer. It is free, arrives in under 5 minutes for most users, and the $5 minimum is among the lowest in the industry. Wire transfers are available for amounts over $10,000. There is no credit card or debit card deposit option.

Interac e-Transfer

This is the method I use and the one most Canadians will use. Minimum deposit is $5 CAD, maximum is $10,000 per transfer. The money typically shows up in your Shakepay account in under 5 minutes, though your bank’s e-Transfer processing time can affect this. No fee on either side.

Wire Transfer

For deposits over $10,000 CAD, wire transfer is the route. Minimum is $10,000 with no maximum listed. Wire transfers can take 1 to 2 business days depending on your bank. Also free on Shakepay’s end, though your bank may charge an outgoing wire fee — check with them first.

Crypto Deposits

You can deposit BTC or ETH directly from another exchange or a hardware wallet. Free, standard blockchain confirmation times apply. Roughly 10 minutes for Bitcoin, faster for Ethereum.

No credit card or debit card deposits are supported. For Canadians who want to buy their first crypto with a card, this rules Shakepay out as the entry point — Coinbase Canada or Wealthsimple would be the options there.

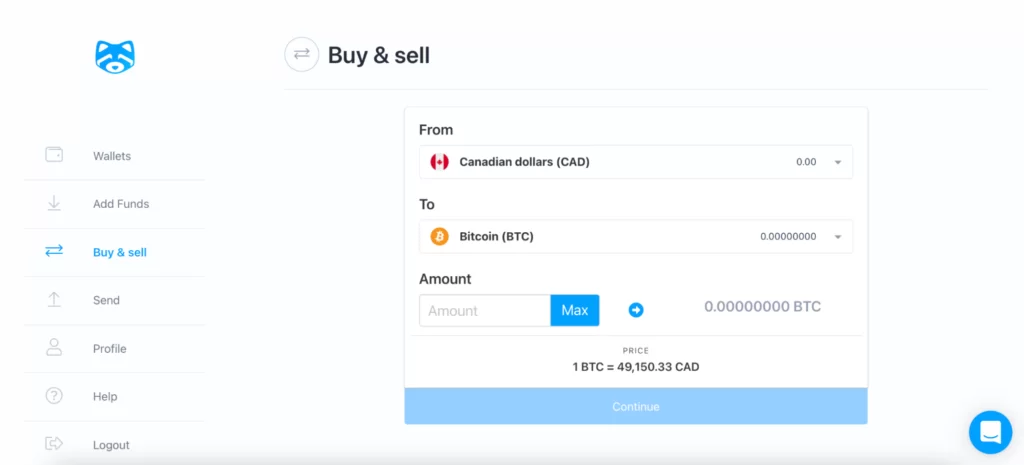

What Does Shakepay Actually Cost? What Are the Real Fees?

Shakepay charges no explicit commission, but it makes money through a spread built into every buy and sell price. That spread typically runs 1.5% to 2.5% depending on market conditions. Deposits, withdrawals (both CAD and crypto), and internal transfers are free. On a $1,000 Bitcoin purchase, you’re paying roughly $15 to $25 more than the market price.

How the Spread Works

When Shakepay shows you a Bitcoin price, it’s already marked up from the market rate. You don’t see a fee line item — you just see a slightly worse price than what’s trading on global markets. That’s the spread. When you sell, the same thing happens in reverse: you get a slightly lower price than market.

I’ve tested this directly. On a $500 buy, the spread cost came out to about $8.50, or 1.7%. That’s consistent with what other reviewers have measured. One independent test put Shakepay’s spread at 2.26% on the day they tested it, which ranked 12th out of 18 platforms in Canada for cost. On smaller amounts it’s barely noticeable. On larger trades or frequent buying, it adds up.

Real Cost Breakdown — What Shakepay Trading Actually Costs You

| Trade Size (CAD) | Estimated Spread Cost | Effective Rate | Notes |

|---|---|---|---|

| $100 | ~$1.50 to $2.50 | 1.5–2.5% | Barely noticeable for occasional buyers |

| $500 | ~$7.50 to $12.50 | 1.5–2.5% | Still acceptable for infrequent buys |

| $1,000 | ~$15 to $25 | 1.5–2.5% | Compare: Newton ~$5–7, NDAX ~$2 |

| $5,000 | ~$75 to $125 | 1.5–2.5% | Large trade optimization may reduce this |

| $10,000+ | Varies | Potentially lower | Contact Shakepay for large trade pricing |

Spread varies with market conditions. Based on published spread range and personal testing. Verified June 17, 2026.

What’s Actually Free

Interac deposits: free. Interac withdrawals: free. Wire transfers: free. Crypto withdrawals (BTC and ETH): free, and Shakepay covers the network mining fees — something most exchanges don’t do. Internal transfers to other Shakepay users via Shaketag: free up to $999 per transfer. These are genuine perks that offset the spread cost for users who aren’t trading constantly.

How Does Shakepay Make Money?

Shakepay markets itself as “commission-free” but earns revenue through the spread between the buy and sell prices it quotes. It is a broker, not an exchange — it sets its own prices rather than matching buyers and sellers. The spread is its primary revenue source, though interest products and eventually loan interest will contribute as well.

The distinction between a broker and an exchange matters for your costs. On a true exchange like Kraken or NDAX, you are buying from another user and the platform takes a small commission. On Shakepay, you are always buying from Shakepay and selling back to Shakepay. The company sets the price. That is how brokers work everywhere: mortgage brokers, currency exchange booths, stock brokerages on simple buy orders. The “no fee” framing is technically accurate but incomplete. The cost is just embedded differently.

That’s not a scam or a hidden fee — it’s how brokers work. But it does mean the “no fee” marketing is a simplification. You’re paying a 1.5–2.5% cost on every trade; it’s just embedded in the price rather than shown as a line item.

As the platform has expanded, new revenue streams have emerged. Shakepay Interest generates revenue on float. Bitcoin-backed loans (launched April 2026 at 9.5% APR) will generate interest income. The Visa card generates interchange revenue. So the spread is still the core, but Shakepay is building a broader financial services model.

What Features Does Shakepay Offer Canadians in 2026?

Shakepay has expanded well beyond a simple Bitcoin broker. In 2026 it offers: BTC and ETH trading, a tiered Visa cashback card, daily BTC rewards via ShakingSats, cash interest up to 3.75% APY, bill payments, direct deposit, USD and USDC accounts, and as of April 2026, bitcoin-backed loans at 9.5% APR.

ShakingSats — Daily Free Bitcoin

Open the app once a day and shake your phone. You get a small amount of satoshis deposited automatically. The more friends you refer, the more you earn per shake. It’s a gamified retention mechanic, but the Bitcoin is real. Long-time users with large referral networks actually accumulate a meaningful amount over time. The ShakeSquad feature lets you form a group of up to four friends who earn rewards on each other’s card spending.

Shakepay Visa Card

A tiered reward system (Base, Bright, Blue) adjusts monthly based on direct deposit activity and trading volume. Base earns 1% BTC cashback, Bright earns 1.25%, and Blue earns 1.5%, with promotional boost windows that can push the rate to 4%. No annual fee, no FX fee, no credit check required. Works with Apple Pay and Google Pay anywhere Visa is accepted. Daily spend limit is $5,000 CAD. ATM withdrawals are excluded from cashback. Rewards settle in BTC directly to your Shakepay balance. I have been using this card for everyday purchases for years. It is the most practical passive way I have found to accumulate small amounts of Bitcoin without changing spending habits. Check our breakdown of crypto Visa cards in Canada for comparisons.

I’ve been using this card for everyday purchases and it remains the most practical way I’ve found to passively accumulate small amounts of Bitcoin without changing my spending habits.

Shakepay Interest

Launched in Q1 2025. Hold Canadian dollars in your Shakepay account and earn up to 3.75% interest annually, paid out in Bitcoin every week. You don’t need to buy BTC to participate — the interest accrues on your CAD balance and converts automatically. It’s the easiest way to start a Bitcoin position without actively timing any purchases.

Bitcoin-Backed Loans (April 2026)

This is the biggest product launch Shakepay has had since the Visa card. You can now borrow against your Bitcoin holdings without selling them. The loan rate is 9.5% APR, capped at $50,000 CAD, and is backed by a 3-year exemptive relief decision from Quebec’s AMF. No client deposits are used to fund the loans. For Canadians who hold Bitcoin and don’t want to trigger a taxable disposition by selling, this opens up a meaningful option — borrow fiat against BTC, spend it, and repay over time while your Bitcoin position stays intact.

Bill Payments, Direct Deposit, USD Accounts

Added throughout 2025: you can now pay utility bills and credit cards directly from your Shakepay balance, set up direct deposit of your paycheque, and hold USD and USDC stablecoins earning up to 3% APY on USD balances. Shakepay is increasingly positioning itself as a full alternative to a traditional bank account for crypto-forward Canadians.

Recurring Buys

Set up automatic BTC or ETH purchases on a schedule. Fund your account, set a weekly or monthly buy amount, and let it run. The best dollar-cost averaging setup Shakepay offers: pair a recurring buy with Shakepay Interest so your cash earns BTC while it sits waiting for the next scheduled purchase. For more on how to buy Bitcoin in Canada, see our guide.

How Does Shakepay Compare to Other Canadian Crypto Platforms?

Shakepay wins on simplicity, Canadian regulatory standing, and unique features like the BTC cashback card and free crypto withdrawals. It loses on trading fees and coin selection. For Canadians who want altcoins or the lowest possible fees on large trades, Newton and NDAX are better options. For Bitcoin-focused users who value a clean experience, Shakepay is the top Canadian pick.

| Exchange | Trading Fees | Coins | CIRO Registered | Key Differentiator | Best For |

|---|---|---|---|---|---|

| Shakepay | 1.5–2.5% spread | 2 (BTC, ETH) | Yes (Jan 2025) | BTC cashback Visa card, free withdrawals, bitcoin loans | Bitcoin beginners, DCA buyers, card spenders |

| Newton | 0.5–0.7% spread | 75+ | Yes | Widest altcoin selection, lowest spread among brokers | Altcoin buyers, cost-conscious traders |

| NDAX | 0.20% flat | 30+ | Yes | Lowest flat fee in Canada, staking, OTC desk | Active traders, low-fee priority |

| Wealthsimple Crypto | 0.5–2% | 100+ | Yes | All-in-one app with stocks, ETFs and crypto | Existing Wealthsimple users, beginners |

| Kraken Canada | 0.40% taker (Kraken Pro) | 250+ | FINTRAC only | Largest coin selection, pro trading tools | Experienced traders, altcoin diversity |

| Bull Bitcoin | ~1.5% spread | BTC only | FINTRAC only | Non-custodial, Bitcoin-only ethos | Self-custody Bitcoin advocates |

Verified June 17, 2026. Exchange status and fees subject to change. Never include Bitbuy — shut down June 2025.

What Are the Biggest Complaints About Shakepay?

The most consistent real complaints about Shakepay fall into three categories: account freezes during deposits, slow customer support when something goes wrong, and the spread being higher than competitors. The Trustpilot score of 1.8/5 is poor, but a significant share of the negative reviews involve third-party scams that targeted Shakepay users — not platform failures.

After going through hundreds of Reddit posts, Trustpilot reviews, and app store feedback, here’s what’s actually going wrong for real users:

Account Freezes During Deposits

This is the most common legitimate complaint and it shows up repeatedly across Trustpilot, Reddit, and the App Store. Users make a CAD deposit via Interac, the funds get flagged for review, and the account gets frozen — sometimes for weeks — while support works through it. This tends to spike during bull markets when new users are signing up in large numbers and anti-money laundering checks get stricter. If you’re depositing large amounts for the first time or making unusual transaction patterns, this is a real risk.

Customer Support Response Times

The support team responds eventually, but “eventually” doesn’t help when your funds are frozen. Email is the main support channel and 24-hour response times are typical under normal conditions. When the platform is busy, that stretches. There is no live chat or phone support.

The Spread Is Higher Than Marketed

Shakepay calls itself “commission-free.” Technically true. But a 1.5–2.5% spread on a $5,000 purchase is $75 to $125 in real money. Some users feel misled when they do the math post-trade. This isn’t a scam — it’s how brokers work — but the framing is aggressive for a platform competing against lower-spread options like Newton.

Third-Party Scams (Not Shakepay’s Fault, but Worth Knowing)

A meaningful portion of the negative reviews on Trustpilot involve people who were scammed by someone pretending to be Shakepay — fake support agents, phishing sites, social media impersonators. These are crimes against Shakepay users, not failures of the platform. But they’re common enough to mention. Shakepay will never initiate contact with you to help you set up your account or deposit money. If anyone contacts you claiming to be Shakepay and asks you to do anything, it’s a scam. Use the official website directly (shakepay.com) and verify any email comes from an @shakepay.com address before clicking anything.

The app store reviews tell a different story than Trustpilot. At 4.7/5 on iOS and 4.5/5 on Google Play with tens of thousands of ratings, the day-to-day experience for most users is clearly positive. The disconnect between the app ratings and the Trustpilot score is explained almost entirely by the fact that happy users leave app reviews and frustrated users leave Trustpilot reviews.

How Is Shakepay’s Customer Support?

Shakepay offers email support through their website and in-app help articles. Based on my personal testing, response time is within 24 hours under normal conditions — acceptable, but not fast. There is no live chat, no phone line, and no weekend guarantee. Users with frozen accounts or verification problems consistently report slower responses and auto-replies that don’t solve the issue.

I have contacted Shakepay support a few times over the years. For straightforward questions about fees or features, they have responded within a day and the answers have been accurate. The experience deteriorates when the issue is account-level. A user whose Interac deposit is frozen is in a different, longer queue than routine support requests, and the communication through that process has been a consistent complaint across r/OCryptoCanada and r/PersonalFinanceCanada.

The support page on their site is genuinely useful for common questions. Most things can be resolved without ever contacting the team. But when you do need a human, the absence of live chat is a real limitation compared to platforms like Wealthsimple Crypto, which has more accessible support infrastructure.

Reddit consensus across r/PersonalFinanceCanada and r/BitcoinCA: people love the app, deal with the spread, and only get frustrated when something unusual happens to their account. As long as you don’t hit an edge case, the experience is smooth.

Who Should Use Shakepay (and Who Shouldn’t)?

Shakepay is the best starting point for Canadians buying Bitcoin for the first time, or for those who want a dead-simple BTC/ETH setup with a useful cashback card. It’s not the right choice for altcoin buyers, active traders watching fees closely, or anyone who wants more than two coins in their portfolio.

Shakepay Is a Good Fit If You:

- Are buying Bitcoin or Ethereum for the first time and want the simplest possible experience

- Want to dollar-cost average into BTC regularly without managing the process actively

- Spend on a card daily and want to earn BTC cashback on that spending without changing habits

- Want to earn interest on idle Canadian dollars sitting in your account

- Hold Bitcoin and want to borrow against it without triggering a taxable disposition

- Regularly move crypto to a hardware wallet and value free network fee coverage

Shakepay Is Not the Right Choice If You:

- Want altcoins beyond BTC and ETH. Try Newton (75+ coins) or Wealthsimple Crypto (100+ coins)

- Trade frequently or in large volumes where the 1.5% to 2.5% spread compounds into serious costs. NDAX at a flat 0.20% is the better option there

- Need to deposit via credit or debit card. Coinbase Canada supports card deposits

- Want live chat or phone support available if something goes wrong

- Are outside Canada. Shakepay is Canadian residents only

Conclusion: Is Shakepay Worth It for Canadians in 2026?

Shakepay is a legitimate, well-regulated, and increasingly full-featured Canadian crypto platform. The spread is higher than the competition and the coin selection is narrow by design — those are real trade-offs. But the combination of free deposits, free crypto withdrawals, a BTC cashback Visa card, cash interest, direct deposit, and now bitcoin-backed loans makes it genuinely useful in ways that go beyond a simple Bitcoin broker.

I’ve watched Shakepay go from a scrappy Montreal startup with 600,000 users and a fun app gimmick to a CIRO-registered financial institution with 1.5 million Canadians and a product suite that looks more like a bank than an exchange. That progression matters. In a space where platforms vanish or get regulated out of existence — and I’ve seen it happen more than once since 2016 — Shakepay’s regulatory track record is a genuine differentiator.

If you are buying Bitcoin for the first time, Shakepay is where I would start. If you are already past the beginner stage and want lower fees or more coins, pair it with Newton or NDAX and keep Shakepay mainly for the card and the free crypto withdrawals. Not sure which exchange fits your situation? Take our exchange quiz.

Ready to get started? Sign up through our link and get $20 free when you trade $100 or more in Bitcoin or Ethereum.

Frequently Asked Questions About Shakepay

Is Shakepay safe for Canadians to use in 2026?

Yes. Shakepay is registered with CIRO as an investment dealer (since January 2025), holds FINTRAC MSB status, and was admitted to Payments Canada in May 2025 as the first crypto-native member. Client funds are held in cold storage with insurance coverage. Two-factor authentication is supported. It is one of the most regulated crypto platforms available in Canada as of June 2026.

Does Shakepay charge fees?

Shakepay charges no explicit commission, but earns through the bid-ask spread on every trade, typically ranging from 1.5% to 2.5% depending on market conditions. CAD deposits, CAD withdrawals, and crypto withdrawals are all free. Shakepay also covers Bitcoin and Ethereum network mining fees — an uncommon perk among Canadian exchanges.

What coins does Shakepay support?

As of June 2026, Shakepay supports only Bitcoin (BTC) and Ethereum (ETH). If you want to buy altcoins, you’ll need a different platform such as Newton, NDAX, or Wealthsimple Crypto.

How does the Shakepay Visa card work?

The Shakepay Visa is a prepaid card with tiered Bitcoin cashback. The base rate is 1% BTC back on all purchases, rising to 1.5% (Blue tier) based on direct deposit and trading activity, with promotional boosts up to 4%. There are no annual fees, no FX fees, and no credit check required. It works with Apple Pay and Google Pay anywhere Visa is accepted in Canada.

Is Shakepay available outside Canada?

No. Shakepay is exclusively for Canadian residents and is available across all 13 provinces and territories.

What are Shakepay’s bitcoin-backed loans?

Launched April 21, 2026, Shakepay’s bitcoin-backed loans allow Canadian residents to borrow fiat currency against their Bitcoin holdings without selling. The loan carries a 9.5% APR, is capped at $50,000 CAD, and is backed by a 3-year exemptive relief decision from Quebec’s AMF. No client deposits are used to fund the loans. This avoids the taxable disposition that a sale would trigger under Canadian tax rules.